If you’re in the market for insurance right now, keep an eye out for scammers in the mix. They’re out in full force once again this open enrollment season.

As people across the U.S. sign up for, renew, or change their health insurance plans, scammers want to cash in as people rush to get their coverage set. And scammers have several factors working in their favor.

For starters, many people find the insurance marketplace confusing, frustrating, and even intimidating, all feelings that scammers can take advantage of. Moreover, concerns about getting the right level of coverage at an affordable price also play into the hands of scammers.

Amidst all this uncertainty and time pressure, health insurance scams crop up online. Whether under the guise of helping people navigate the complex landscape or by offering seemingly low-cost quotes, scammers prey on insurance seekers by stealing their personal information, Social Security numbers, and money.

According to the FBI, health insurance scams cost families millions each year. In some cases, the costs are up front. People pay for fraudulent insurance and have their personal info stolen. And for many, the follow-on costs are far worse, where victims go in for emergency care and find that their treatment isn’t covered—leaving them with a hefty bill.

Like so many of the scams we cover here in our blogs, you can spot health insurance scams relatively quickly once you get to know their ins and outs.

What Kind Of Health Insurance Scams Are Out There Right Now?

Here’s how some of those scams can play out.

The Phishing Strategy

Some are “one and done scams” where the scammer promises a policy or service and then disappears after stealing money and personal info—much like an online shopping scam. It’s a quick and dirty hit where scammers quickly get what they want by reaching victims the usual ways, such as through texts, emails, paid search results, and social media. In the end, victims end up on a phishing site where they think they’re locking in a good deal but handing over their info to scammers instead.

The Long Con

Other scams play a long con game, milking victims for thousands and thousands of dollars over time. The following complaint lodged by one victim in Washington state provides a typical example:

A man purchased a plan to cover himself, his wife, and his two children, only to learn there was no coverage. He was sold a second policy, with the same result, and offered a refund if he purchased a third policy. When he filed a complaint, his family still had no coverage, and he was seeking a refund for more than $20,000 and reimbursement for $55,000 in treatments and prescriptions he’d paid out of pocket.

Scams like these are known as ghost broker scams where scammers pose as insurance brokers who take insurance premiums and pocket the money, leaving victims thinking they have coverage when they don’t. In some cases, scammers initially apply for a genuine policy with a legitimate carrier, only to cancel it later, while still taking premiums from the victim as their “broker.” Many victims only find out that they got scammed when they attempt to file a claim.

The “Fake” Cancellation Scam

Another type of scam comes in the form of policy cancellation scams. These work like any number of other account-based scams, where a scammer pretends to be a customer service rep at a bank, utility, or credit card company. In the insurance version of it, scammers email, text, or call with some bad news—the person’s policy is about to get cancelled. Yet not to worry, the victim can keep the policy active they hand over some personal and financial info. It’s just one more way that scammers use urgency and fear to steal to commit identity theft and fraud.

What Are The Signs Of A Health Insurance Scam?

As said, health insurance scams become relatively easy to spot once you know the tricks that scammers use. The Federal Trade Commission (FTC) offers up its list of the ones they typically use the most:

1)Someone says they’re from the government and need money or your personal info.Government agencies don’t call people out of the blue to ask them for money or personal info. No one from the government will ask you to verify your Social Security, bank account, or credit card number, and they won’t ask you to wire money or pay by gift card or cryptocurrency.

If you have a question about Health Insurance Marketplace®, contact the government directly at: HealthCare.gov or 1-800-318-2596

2) Someone tries to sell you a medical discount plan. Legitimate medical discount plans differ from health insurance. They supplement it. In that way, they don’t pay for any of your medical expenses. Rather, they’re membership programs where you pay a recurring fee for access to a network of providers who offer their services at pre-negotiated, reduced rates. The FTC strongly advises thorough research before participating in one, as some take people’s money and offer very little in return. Call your caregiver and see if they really participate in the program and in what way. And always review the details of any medical discount plan in writing before you sign up.

3) Someone wants your sensitive personal info in exchange for a price quote. The Affordable Care Act’s (ACA’s) official government site is HealthCare.gov. It lets you compare prices on health insurance plans, check your eligibility for healthcare subsidies, and begin enrollment. But HealthCare.gov will only ask for your monthly income and your age to give you a price quote. Never enter personal financial info like your Social Security number, bank account, or credit card number to get a quote for health insurance.

4) Someone wants money to help you navigate the Health Insurance Marketplace. The people who offer legitimate help with the Health Insurance Marketplace (sometimes called Navigators or Assisters) are not allowed to charge you and won’t ask you for personal or financial info. If they ask for money, it’s a scam. Go to HealthCare.govand click “Find Local Help” to learn more.

How to Avoid Health Insurance Scams

1)For health insurance, visit a trusted source like HealthCare.gov or your state marketplace. Doing so helps guarantee that you’ll get the kind of fully compliant coverage you want.

2) Make sure the insurance covers you in your state. Not every insurer is licensed to operate in your state. Double-check that the one you’re dealing with is. A good place to start is to visit the site for your state’s insurance commission. It should have resources that let you look up the insurance companies, agents, and brokers in your state.

3) For any insurance, research the company offering it. Run a search with the company name and add “scam” or “fraud” to it. See if any relevant news or complaints show up. And if the plan you’re being offered sounds too good to be true, it probably is.

4) Watch out for high-pressure sales. Don’t pay anything up front and be cautious if a company is forcing you to make quick decisions.

5) Guard your personal info. Never share your personal info, account details, or Social Security number over text or email. Make sure you’re really working with a legitimate company and that you submit any info through a secure submissions process.

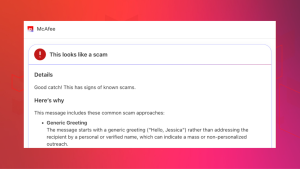

6) Block bad links to phishing sites. Many insurance scams rely on phishing sites to steal personal info. A combination of our Web Protection and Scam Detector can steer you clear of them. They’ll alert you if a link might take you to one. It’ll also block those sites if you accidentally tap or click on a bad link.

7) Monitor your identity and credit. In some health insurance scams, your personal info winds up in wrong hands, which can lead to identity fraud and theft. And the problem is that you only find out once the damage is done. Actively monitoring your identity and credit can spot a problem before it becomes an even bigger one. You can take care of both easily with our identity monitoring and credit monitoring.

Additionally, our identity theft coverage can help if the unexpected happens with up to $2 million in identity theft coverage and identity restoration support if determined you’re a victim of identity theft.

You’ll find these protections and more in McAfee+.

Stay Updated

Follow us to stay updated on all things McAfee and on top of the latest consumer and mobile security threats.