Can AI Hack People Now? What the Reported Hugging Face Cyberattack Means

Jul 31, 2026 | 3 MIN READ

Ghost Tapping: What It Is, How It Works, and How to Stay Safe

Contactless payments make everyday purchases fast and easy. Yet with that convenience comes a risk: ghost tapping....Jul 27, 2026 | 5 MIN READ

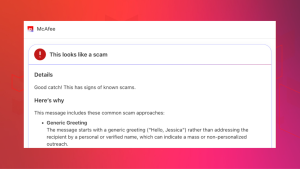

How to Use Claude with McAfee to Check “Is This a Scam?”

Use Claude with McAfee to check suspicious links, messages, and screenshots in seconds. Learn how this new integration helps you...Jul 20, 2026 | 5 MIN READ

How to Know If Your Phone Has Been Hacked

It’s often pretty easy to tell when a piece of your tech isn’t working quite right. The...Jul 07, 2026 | 15 MIN READ

Can AI Hack People Now? What the Reported Hugging Face Cyberattack Means

Reports say autonomous AI models were involved in a cyberattack targeting AI platform Hugging Face. Here's what reportedly happened, why...Jul 31, 2026 | 3 MIN READ

Ghost Tapping: What It Is, How It Works, and How to Stay Safe

Contactless payments make everyday purchases fast and easy. Yet with that convenience comes a risk: ghost tapping....Jul 27, 2026 | 5 MIN READ

Chick-fil-A Data Breach Explained: What Customers Need to Know

Hackers targeted Chick-fil-A loyalty accounts in a credential stuffing hack using stolen usernames and passwords. Learn what happened and how...Jul 24, 2026 | 3 MIN READ

Can AI Hack People Now? What the Reported Hugging Face Cyberattack Means

Reports say autonomous AI models were involved in a cyberattack targeting AI platform Hugging Face. Here's what reportedly happened, why...Jul 31, 2026 | 3 MIN READ

How to Use Claude with McAfee to Check “Is This a Scam?”

Use Claude with McAfee to check suspicious links, messages, and screenshots in seconds. Learn how this new integration helps you...Jul 20, 2026 | 5 MIN READ

The FaceTime Bank Scam That Can Expose Your Passwords in Real Time: This Week in Scams

Scammers don’t always need sophisticated malware to steal your money. Increasingly, they’re relying on something much simpler: your trust. This week, fraudsters...Jul 17, 2026 | 4 MIN READ

Can AI Hack People Now? What the Reported Hugging Face Cyberattack Means

Reports say autonomous AI models were involved in a cyberattack targeting AI platform Hugging Face. Here's what reportedly happened, why...Jul 31, 2026 | 3 MIN READ

Chick-fil-A Data Breach Explained: What Customers Need to Know

Hackers targeted Chick-fil-A loyalty accounts in a credential stuffing hack using stolen usernames and passwords. Learn what happened and how...Jul 24, 2026 | 3 MIN READ

How to Use Claude with McAfee to Check “Is This a Scam?”

Use Claude with McAfee to check suspicious links, messages, and screenshots in seconds. Learn how this new integration helps you...Jul 20, 2026 | 5 MIN READ

Can AI Hack People Now? What the Reported Hugging Face Cyberattack Means

Reports say autonomous AI models were involved in a cyberattack targeting AI platform Hugging Face. Here's what reportedly happened, why...Jul 31, 2026 | 3 MIN READ

Chick-fil-A Data Breach Explained: What Customers Need to Know

Hackers targeted Chick-fil-A loyalty accounts in a credential stuffing hack using stolen usernames and passwords. Learn what happened and how...Jul 24, 2026 | 3 MIN READ

How to Use Claude with McAfee to Check “Is This a Scam?”

Use Claude with McAfee to check suspicious links, messages, and screenshots in seconds. Learn how this new integration helps you...Jul 20, 2026 | 5 MIN READ

Can AI Hack People Now? What the Reported Hugging Face Cyberattack Means

Reports say autonomous AI models were involved in a cyberattack targeting AI platform Hugging Face. Here's what reportedly happened, why...Jul 31, 2026 | 3 MIN READ

Chick-fil-A Data Breach Explained: What Customers Need to Know

Hackers targeted Chick-fil-A loyalty accounts in a credential stuffing hack using stolen usernames and passwords. Learn what happened and how...Jul 24, 2026 | 3 MIN READ

How to Use Claude with McAfee to Check “Is This a Scam?”

Use Claude with McAfee to check suspicious links, messages, and screenshots in seconds. Learn how this new integration helps you...Jul 20, 2026 | 5 MIN READ

Take control with McAfee+ Advanced

Full-service identity and credit protection now in one plan

Get McAfee+ Advanced