What’s blockchain technology? The term gets bandied about often enough, but it doesn’t always get the explanation it deserves.

Understanding the basics of blockchain can help you understand several of the big changes that are taking place online. It’s the foundational technology that underpins cryptocurrency and NFTs (non-fungible tokens), yet it has several other emerging applications as well.

In all, gaining a sense of how blockchain technology works will give you a further sense as to how it may eventually shape the way you go about your day.

Blockchain technology holds great potential because of the unique, decentralized way it handles data—which marks the first step in understanding how it works.

How blockchains work

An easy way to visualize how a blockchain works is with an old-fashioned ledger. Each ledger entry is a link in a “chain.” Within each chain is a unique identifier known as a hash and a block of data associated with it. Over time, chains get added, which updates the hash as new blocks of data are added to the chain.

A simplified example of a blockchain storing recipe instructions. The Previous Hash and Stuff (data) fields generate the Hash field. This Hash becomes part of the next record.

Yet one of the most important aspects of blockchain technology is this—it’s decentralized. Dozens, hundreds, thousands, or more participants in the blockchain track and validate the transactions associated with it.

Each blockchain entry gets validated through consensus, where individual participants on a blockchain network must all “agree” that the data in each entry is correct. Participants in the blockchain network can arrive at consensus through several models, yet commonly they use cryptographic calculations to validate an update to the chain.

In this way, blockchain technology removes the need for a central authority to oversee a transaction, such as a bank. Put simply, blockchain gets rid of the go-between. And it makes transactions more anonymous as a result.

Participants in a blockchain network receive a small amount of cryptocurrency per transaction as a reward for their efforts. Enter the notion of crypto mining, where some miners set up large-scale farms of powerful, specialized computers that participate in blockchain networks.

Blockchains come in public and private forms. Public is just as it sounds, where anyone can participate in the blockchain. They can read, write, or validate data in the blockchain. Private blockchains are invite-only in nature and can establish rules about who can alter the blockchain.

Many blockchain ledger entries record financial transactions associated with cryptocurrency. However, ledger entries can contain any type of data. One can just as easily store documents, images, log files, or other items in a blockchain. Even decentralized programs, also known as smart contracts, can be stored.

In all, there’s much more to blockchain technology than just cryptocurrency.

How are blockchains used? Real-world applications of blockchain.

First and foremost, blockchain technology is at the heart of cryptocurrency. Wherever cryptocurrency is bought, spent, or exchanged, the blockchain is there to facilitate the transaction. However, we can point to several new and emerging applications as well, including:

- NFTs: Another popular application of blockchain technology is NFTs (non-fungible tokens), which are often used to record and transfer ownership of digital assets. Examples include .jpeg images of artwork, videos, or even tweets, such as the one that former Twitter CEO Jack Dorsey sold for $2.9 million.

- Transfer of real-world goods: Just as digital goods can be bought and sold via blockchain, so can things such as vehicles and property. Blockchain can verify the original owner, the sale, and then the transfer of ownership to the party who made the purchase.

- Healthcare and science applications: Doctors and researchers are now exploring blockchain technologies as a means of gathering, validating, and sharing medical data securely.

- Supply chain monitoring: The ledger-like entries make blockchain technology ideal for tracking the progress of goods as they make their way to consumers. Auto companies are exploring this technology to manage their vendors and the manufacturing process overall. Likewise, it has applications in agriculture as food is tracked along its supply chain across growers, shippers, wholesalers, retailers, and ultimately to shoppers.

- 5G data: Businesses, organizations, and cities will increasingly adopt 5G-enabled devices to monitor everything from heating systems in buildings, medical equipment, and traffic signals. Blockchain technology can help verify the authenticity of the data these devices will exchange—particularly for the 5G-enabled devices that will help run critical infrastructure and business operations.

The pros and cons of blockchain technology

Blockchain technology offers several benefits, yet it has its downsides as well.

Decentralization removes the need for third parties in transactions because the blockchain provides the verification and oversight for the transaction to go through. In the case of financial transactions, that removes the need for banks. In the sale of property, that removes the need for a title company.

However, if there is a conflict or issue between the parties, they have no central authority to manage its resolution. (See this story written by a BBC journalist about his quest to recover stolen crypto funds.)

Additionally, decentralization can afford parties anonymity, which can cover up illegal activities—thus making cryptocurrency is the coin of the realm for scammers and murky marketplaces on the dark web.

Blockchain technology is open, meaning that theoretically anyone with a specially equipped device can generate revenue as a miner in the blockchain economy. Yet the reality is that much of the technology is in the hands of the few. For starters, these mining devices are expensive. Secondly, it takes hundreds of these devices to mine effectively, which points to the advent of the industrial-sized mining farms mentioned above.

To put it all into perspective, one study estimated that “(t)he top 10% of [Bitcoin] miners control 90% and just 0.1% (about 50 miners) control close to 50% of mining capacity.”

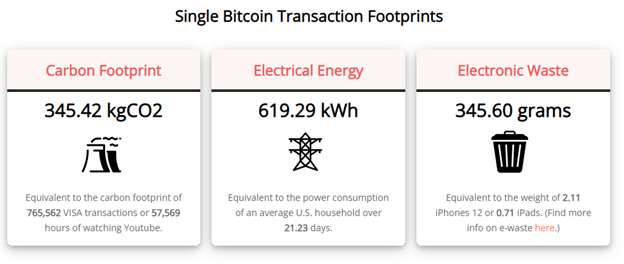

Additionally, all that computing power comes at an additional cost—energy. It takes electricity to run those huge mining farms, and it takes yet more electricity to keep them cool. As a result, crypto mining can generate an outsized carbon footprint if the electricity is generated with fossil fuels.

Image and data courtesy of Digiconomist

Of note, the second-largest cryptocurrency, Ethereum has made great strides on the energy consumption front. It updated the way the cryptocurrency arrives at consensus in its blockchain and uses far less energy as a result. Estimates show that Ethereum’s carbon footprint decreased by about 99.992% from 11,016,000 to 870 metric tons of CO2.

The future of blockchain technology

As far as technology goes, we still live in the relatively early days of blockchain. And while much of its popular focus revolves around its role in cryptocurrencies like Bitcoin, the technology offers more than that. Of course, it remains to be seen which of its applications will take root.

Blockchain has its own barriers, though, particularly when it comes to security. Like any other connected technology, it finds itself the target of hacks and attacks. Billions of dollars in cryptocurrency have been stolen from individual users and exchanges over the years.

The security issue isn’t necessarily with the blockchain itself. That’s highly difficult to hack thanks to encryption and the decentralized nature of the blockchain. Instead, the networks they are on are subject to attack—such as interception attacks where bad actors extract information or cryptocurrency. Other attacks involve flooding the blockchain network with false identities that ultimately crash the system. And yet more exploit weaknesses in the security protocols used by platforms like cryptocurrency exchanges.

Then there’s the tried-and-true phishing attack, where scammers dupe victims into handing over their personal encryption keys. With a key, the scammer can empty digital wallets of their cryptocurrency or compromise a private blockchain network and that data in it.

Clearly, the future remains speculative as people and organizations explore the uses of blockchain technology. Without question, security will play a major role in its adoption.

What does blockchain mean for everyday internet users?

Unless you’re dabbling in cryptocurrency yourself, blockchain will likely remain a behind-the-scenes technology. At least for the time being.

Yet it can still shape your day in some way. It might help bring fresher produce to your market. It might secure smart utilities and smart infrastructure in your city. And it might give your auto manufacturer a powerful tool for identifying and recalling a faulty part in your car.

Although barriers of security, energy consumption, and equity remain, it stands a good chance that blockchain technology will continue to change our lives. And understanding how it works can help you better understand those changes.

Stay Updated

Follow us to stay updated on all things McAfee and on top of the latest consumer and mobile security threats.